Executive Summary

On 18 February 2022, Finance Minister Mr. Lawrence Wong delivered his budget speech for fiscal year April 2022 to March 2023 in Parliament. The theme of the budget this year is “Charting Our New Way Forward Together”.

In this budget, the Government announced Singapore’s strategic directions for growth in a fast-changing, post pandemic world that address issues of climate change, digitalisation, wealth inequalities and demographic challenges. Signs of Singapore’s commitment to long-term investment in the future are reflected in an expansionary budget that invests in skills and capabilities in tandem with an accelerated green transition and notable tax reforms.

The 3 key thrusts of the budget include investing in new capabilities, advancing our green transition, and renewing and strengthening our social compact. These key trusts reflect a fiscal policy approach that has shifted from addressing the immediate COVID-19 crisis to a long-term view intended to support Singapore in the way forward. Reforms aimed at creating a resilient tax system featured heavily in this budget, with reforms announced across both corporate (direct tax and GST) and personal taxes. On the international tax front, Minister Lawrence Wong highlighted the need to update Singapore’s corporate tax system due to global tax developments – relating to the Base Erosion and Profit Shifting initiative, or BEPS 2.0.

Finally, on the Goods and Services Tax front, the planned GST hike has been delayed to 2023, with the increase to be staggered in two steps. The first increase from 7% to 8% will take place on Jan 1, 2023, and the second increase from 8% to 9% will take place Jan 1, 2024.

Below, we summarise the key tax changes announced in Budget 2022:

1. Changes to Corporate Tax

A major change to our tax system is on the horizon. This is a direct response to a global political agreement that was reached in October 2021 to implement a minimum corporate tax rate of 15% on large multinational groups (i.e. those with a minimum annual revenue of €750 mil, as reflected in the consolidated financial statements of the ultimate parent entity). In response, Singapore will explore a top-up tax called the Minimum Effective Tax Rate, which will top-up multinational enterprise groups’ effective tax rate in Singapore to 15%. The eventual form of the rule Singapore implements will depend on the global implementation framework, reactions from other jurisdictions and widespread industry consultation. It is also premature at this point to speculate on the timing of implementation; OECD has set an aggressive global deadline of 1 Jan 2023, but this appears extremely unlikely.

Meanwhile, there will be no immediate change to the corporate tax rate of 17% or the partial tax exemption scheme which applies to the first $200,000 of a company’s normal chargeable income. Consistent with Year of Assessment (“YA”) 2021, no corporate income tax rebate will be granted for YA 2022.

For comparison, we append below corporate tax rates for selected jurisdictions:

|

Jurisdiction |

Corporate Tax Rate (%) |

Jurisdiction |

Corporate Tax Rate (%) |

| Hong Kong | 16.5 | Vietnam | 20 |

| Taiwan | 20 | China | 25 |

| Thailand | 20 | The Philippines | 30 |

| South Korea | 25 | India | 30 |

| Indonesia | 20 | Japan | 30.62 |

| Malaysia | 24 |

2. Goods and Services Tax

2.1 Update of the GST treatment for travel arranging services

Currently, the GST treatment of travel arranging services provided by local suppliers is based upon where the transportation takes place and where the accommodation is located. With effect from 1 January 2023, the GST treatment will be updated to be based on the belonging status of the contracting party and party directly benefiting from the service. IRAS will be providing further details on the changes by 31 July 2022.

2.2 Facilitating disclosure of company-related information for official duties

Currently, IRAS can only disclose information it has collected to a public officer for the performance of official duties when taxpayers have provided consent. Going forward, to support data-driven policymaking, operations, and integrated service delivery, changes will be made to facilitate IRAS’ disclosure of a prescribed list of identifiable information on companies to public sector agencies for the performance of official duties, without requiring taxpayer consent. Any such information shared will be made less granular by IRAS to preserve the taxpayer’s confidentiality.

3. Extensions and Enhancements to Tax Schemes

3.1 Extension of the broad-based withholding tax (“WHT”) exemption for container lease payments made to non-tax-resident lessors under operating lease (“OL”) agreements

Currently, WHT exemption is allowed on container lease payments made to non-tax-resident lessors (excluding payments derived by the non-tax-resident through its permanent establishment in Singapore) under OL agreements for the use of qualifying containers for the carriage of goods by sea. This exemption – which was scheduled to lapse after 31 December 2022 – will be extended to 31 December 2027.

3.2 Extension of the broad-based WHT exemption for ship and container lease payments under finance lease (“FL”) agreements for Maritime Sector Incentive (“MSI”) recipients

Currently, WHT exemption is allowed on ship and container lease payments made to non-tax-resident lessors (excluding payments derived by the non-tax-resident through its permanent establishment in Singapore) under FL agreements for specified MSI recipients. This exemption – which was scheduled to lapse after 31 December 2023 – will be extended to FL agreements entered into on or before 31 December 2028.

3.3 Extension of the Aircraft Leasing Scheme (“ALS”)

Under the ALS, approved aircraft lessors and aircraft investment managers enjoy tax benefits including concessionary tax rates on qualifying income and automatic WHT exemption on qualifying payments made by approved aircraft lessors to non-tax-residents in respect of qualifying loans and finance leases entered into on or before 31 December 2022. The ALS – which was scheduled to lapse after 31 December 2022 – will be extended to 31 December 2027.

3.4 Extension and enhancement of the Approved Royalties Incentive (“ARI”)

Currently, tax exemption or a concessionary WHT rate may be granted on approved royalties, technical assistance fees, or contributions to research and development costs made to a non-tax-resident for providing cutting-edge technology and know-how. Approval is granted on an agreement-based approach. This incentive – which was scheduled to lapse after 31 December 2023 – will be extended to 31 December 2028 and enhanced to an activity, set-based approach. EDB will be providing further details of the changes by 30 June 2022.

3.5 Extension of the Approved Foreign Loan (“AFL”) scheme

The AFL scheme was introduced to encourage companies to invest in productive equipment for the purpose of conducting substantive activities in Singapore. Under the scheme, tax exemption or a concessionary WHT rate may be granted on interest payments made to a non-tax-resident for loans to a company to purchase productive equipment. The AFL scheme – which was scheduled to lapse after 31 December 2023 – will be extended to 31 December 2028.

3.6 Enhancement of the Tax Incentive Scheme for Funds Managed by Singapore-based Fund Manager (“Qualifying Funds”)

Qualifying Funds, comprising basic tier funds (sections 13D and 13O schemes) and enhanced tier funds (section 13U scheme), are granted tax exemption on specified income (“SI”) derived from designated investments (“DI”), subject to conditions. The DI currently includes physical commodities that are subject to conditions. Going forward, these conditions will be refined. MAS will release further details of all changes by 31 May 2022.

3.7 Extension and Rationalisation of the Withholding Exemption for Financial Sector

The withholding tax exemption applicable to financial institutions to non-resident persons for interest rate or currency swap transactions and specified payments made under securities lending or repurchase agreements – which was scheduled to lapse after 31 December 2022 – will be extended to cover payments made under any contract or agreement that takes effect on or before 31 December 2026. MAS will release consequential changes by 31 May 2022.

3.8 Extension and Rationalisation of Tax Incentives for Project and Infrastructure Finance

The package of tax incentive schemes for Project and Infrastructure Finance, which includes exemptions of qualifying income from qualifying project debt securities (“QPDS”) and an exemption of qualifying foreign sourced income from qualifying offshore infrastructure projects/assets received by approved entities listed on the Singapore Exchange (“SGX”), was scheduled to lapse on 31 December 2022. This will be extended to 31 December 2025. The concessionary tax rate of 10% on qualifying income derived by an approved Infrastructure Trustee Manager/Fund Management Company from managing qualifying SGX-listed Business Trusts/Infrastructure funds in relation to qualifying infrastructure projects/assets (“ITMFM scheme”) will be permitted to lapse on 31 December 2022.

MAS will release additional details on the changes by 31 May 2022.

3.9 Integrated Investment Allowance (“IIA”) scheme to lapse after 31 December 2022

The IIA scheme grants a qualifying company an additional allowance on fixed capital expenditure incurred for qualifying productive equipment placed overseas for approved projects. The IIA scheme will be allowed to lapse after 31 December 2022.

4. Tax Changes for Insurance Sector

4.1 Extension of the Tax Framework for Facilitating Corporate Amalgamations under section 34C of the ITA to Licensed Insurer

The tax framework under section 34C of the ITA treats qualifying corporate amalgamations as a continuation of the existing businesses of the amalgamating companies by the amalgamated company for tax purposes. The tax framework that minimise the tax consequences arising from a qualifying corporate amalgamation has been extended to companies in the insurance business, subject to conditions and modifications as appropriate. IRAS will provide further details of the changes by 31 October 2022.

4.2 Change in the basis of preparation of tax computations from insurers from financial statements (“FS”) to MAS Statutory Returns

Insurers generally rely on FS prepared in accordance with the accounting standards as the basis for preparing their tax computations. With the adoption of the new Financial Reporting Standard (“FRS”) 117 for the preparation of FS, the MAS Statutory Returns (i.e. insurance returns filed with MAS for regulatory purposes) – rather than FS – will be used as the basis for preparing tax computations for insurers. IRAS will provide further details of the changes by 30 September 2022.

5. Other Tax Changes

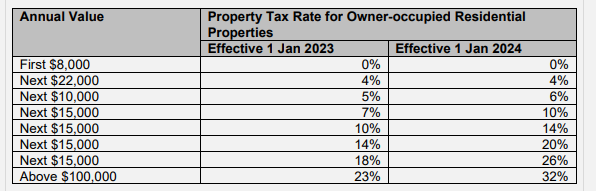

5.1 Enhancement of the progressivity of property tax for owner-occupied residential properties

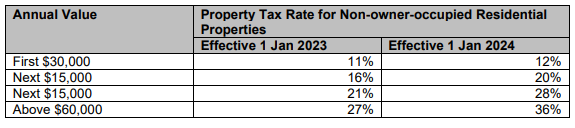

5.2 Enhancement of the progressivity of property tax for non-owner-occupied residential properties

Property tax rates will be increased for non-owner-occupied residential properties with annual value in excess of $30,000. Rates will be increased in two phases, from 1 January 2023 and 1 January 2024, with 36% property tax payable in the highest bracket (annual value >$60,000) effective 1 January 2024. In comparison, currently, the highest property tax rate of 20% applies to properties with annual value in excess of $90,000. This change phased in over two years as shown below:

5.3 Extension of the WHT tax exemption for non-tax-resident mediators and arbitrators

Non-tax-resident professionals are subject to WHT tax at a rate of 15% on gross income from the profession; or they may elect to be taxed at 22% on net income. As a concession, subject to conditions, income derived by non-tax-resident mediators and arbitrators from work carried out in Singapore is exempt from tax. This exemption – which was scheduled to lapse after 31 March 2022 – will be extended till 31 March 2023.

From 1 April 2023 till 31 December 2027, gross income derived by non-tax-resident arbitrators and mediators will be subject to a concessionary WHT tax rate of 10%, or they may elect to be taxed at 24% on net income, from YA 2024 onwards.

5.4 New Additional Registration Fee (“ARF”) tier for cars

A new ARF tier will be introduced for vehicles with open market value in excess of $80,000 with an ARF rate of 220% of the Open Market Value (“OMV”) of the vehicle. In comparison, currently, the highest ARF tier of 180% applies to vehicles with OMV in excess of $50,000

5.5 Increased Carbon Tax

Carbon tax will be increased from $5 per tonne of emissions to $50-$80 by 2030, in addition to ramping the up Singapore’s decarbonisation pathway.

6. Changes to Individual Income Tax – Personal Income Tax Rates

With effect from YA 2024, two new tax brackets will be introduced for tax-resident individuals with chargeable income in excess of 0.5 mil to 1 mil respectively. For resident taxpayers below this bracket, personal tax rates remain unchanged from YA 2017. We append below the tax rate table for resident taxpayers:

Tax rate structure with effect from Year of Assessment (“YA”) 2024

|

Chargeable Income |

Tax Rate (%) |

Gross Tax Payable |

Chargeable Income |

Tax Rate |

Gross Tax Payable |

|

|

On the first On the next |

20,000 10,000 |

0 2 |

0 200 |

200,000 40,000 |

– 19 |

21,150 7,600 |

|

On the first On the next |

30,000 10,000 |

– 3.5 |

200 350 |

240,000 40,000 |

– 19.5 |

28,750 7,800 |

|

On the first On the next |

40,000 40.000 |

– 7 |

550 2,800 |

280,000 40,000 |

– 20 |

36,550 8,000 |

|

On the first On the next |

80,000 40,000 |

– 11.5 |

3,350 4,600 |

320,000 180,000 |

– 23 |

44,550 39,600 |

|

On the first On the next |

120,000 40,000 |

– 15 |

7,950 6,000 |

500,000 180,000 |

– 23 |

84,150 115,000 |

|

On the first On the next |

160,000 40,000 |

– 18 |

13,950 7,200 |

1,000,000 1,000,000 |

– 24 |

199,150 |

7. Year of Assessment 2022 tax filing due dates

We wish to take this opportunity to remind our clients of the tax filing due dates for the Year of Assessment 2022:

Personal Tax filing due on 18 April 2022 (By e-filing)

Partnerships, Clubs, filing due on 15 April 2022

Associations and

Management Corporations

Corporate Tax filing due on 30 November 2022